Lloyds of London Annual Results and what it means for your business

Lloyd’s of London has recently unveiled its highly anticipated annual results for 2023, offering a comprehensive insight into the current state and future trajectory of the insurance market.

The annual report: A closer look

Before we get into the results, it’s important to mention that an insurance company drives profits in two ways:

- Underwriting performance: An insurer endeavours to collect more in premiums than they spend in claims and operating costs.

- Investment performance: They invest that premium until such time as they need to pay out claims.

In 2023, the Lloyd’s market showcased its resilience with a robust underwriting result of £5.9bn, a significant leap from £2.6bn in 2022. This achievement was accentuated by an impressive combined ratio of 84%, reflecting a remarkable 7.9% enhancement over the previous year. This has marked their best underwriting performance in recent history (the best since 2007). The underwriting success was driven by reduced costs stemming from large losses and natural catastrophe claims.

Furthermore, Lloyd’s achieved a noteworthy profit before tax of £10.7bn, a remarkable turnaround from the £0.8bn loss reported in 2022.

Lloyd’s commitment to enhancing performance and reducing the costs of doing business with them has yielded a 0.1% reduction in the attritional loss ratio* now standing at 48.3%. Alongside this, the expense ratio has remained stable at 34.4%, mirroring the disciplined approach to cost management.

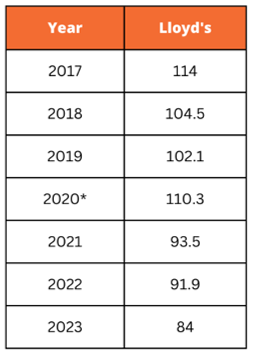

Lloyd’s Combined Ratio: Throughout the years.

The best measure of a successful insurer is its underwriting performance. This is simply assessed by a common ratio called the “Combined Ratio”. The combined ratio is a metric for evaluating the profitability and financial health of an insurance company. To get the combined ratio, you divide the total sum of incurred losses and expenses by the earned premium. So, a combined ratio of 100% is breakeven (before taking into account investment returns). Conversely, a combined ratio of 95% essentially means an underwriting profit of 5% of premium.

As mentioned, the combined ratio in 2023 was 84%, providing a highly profitable result. See below the combined ratios throughout the years.

*Impacted by COVID

*Attritional loss ratio definition – The measure of residual insurance claims as a percentage of earned premiums (net of reinsurance). Attritional insurance claims are calculated as total claims with major losses and movements in prior year claims reserves subtracted.

*Source: Llloyd’s 2023 Full Year Results

For a deeper dive into the Lloyd’s of London results, view the full report here.

Word on the street: How will this transfer to our clients?

PNO visits Lloyds twice a year, and at the time of writing, we are currently nearing the end of a week of meetings with Lloyds underwriters before making our way to Singapore.

So “the word on the street” is that despite the undeniable success of the past year, Lloyd’s underwriters are warily attributing the positive results to two key factors:

- An inflated investment income, with “mark to market” adjustments to some assets

- An abnormally quiet natural catastrophe loss season worldwide.

In saying this, there is strong optimism within the Property market and Lloyds insurers and syndicates are offering more capacity for the Australian market both directly and through MGA’s (including current and new Insurers).

They believe that the remediation efforts undertaken over the past 4-5 years were imperative and that rates should now stabilise, with some slight reductions due to competition from the additional capacity on well-run, good risk-managed accounts.

“Australia is renowned for bouncing in and out of Lloyds markets”

Insurers are concerned that risks will be transferred back from Lloyds to local capacity within Australia, which we feel is a short-sighted approach, particularly in regard to high-hazard industries as Australia needs this market to remain open.

To counter this, some Lloyds Insurers are opening Australian based retail arms, which we welcome.