Underinsurance occurs when you’ve taken out insufficient insurance to cover the replacement value of your property. Often, policy holders find themselves underinsured because they have not been increasing their sum insured at the same rate that construction costs have risen.

Examples of some common causes for underinsurance:

- Increased building costs

- Unknown supplementary costs (costs of demolition, clean up, architect and surveyor fees)

- Not accounting for upgrades to your property

- Estimating your sum insured low to reduce premium costs

How will the insurer respond in the event of a claim?

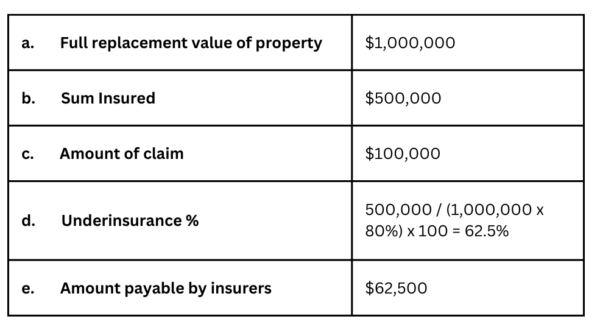

*It’s important to note that most insurers do allow a margin of undervaluation, typically between 80% – 90%, depending on their policy wording. We have used 80% in the below example.

Below is a simple example to illustrate the application and effect of the underinsurance:

You insure your property for $500,000 (Sum Insured). An insured event occurs, such as a fire or flood, causing $100,000 worth of damage to the property.

An insurer determines that the full replacement value of your property is $1,000,000.

As you have insured your property for $500,000, you have underinsured yourself by 37.5%.

Therefore, at claim time, you will only be insured for 62.5% of the value, meaning the amount payable by insurers will then only be $62,500, and not the full $100,000 you have claimed for.

What is the impact of underinsurance?

The major impact of underinsurance is that at claim time, it could lead to needing to contribute to the cost of repairs or rebuild out of your own pocket.

Looking at the previous example, in this particular scenario, the policy holder is responsible for paying for 37.5% of the claim, resulting in contributing $37,500 of their own funds.

How to prevent underinsurance?

Property owners can take proactive measures to prevent underinsurance, typically involving essential due diligence when purchasing or reviewing an insurance policy.

Here are some effective methods for accurately assessing replacement value:

- Organise a formal valuation for insurance purposes

- Talk to a builder with relevant expertise in your type of building

- Engage with your broker who has some basic valuation tools

A bank valuation can also serve as a valuable resource. However, it’s important to note that insurance policies represent replacement cost rather than a purchase price. Furthermore, bank valuations encompass both land and property, whereas land is typically not insured.

If you’d like to find out more or would like to review your insurance policy, please contact mlethborg@pno.com.au or speak with your broker at PNOinsurance.